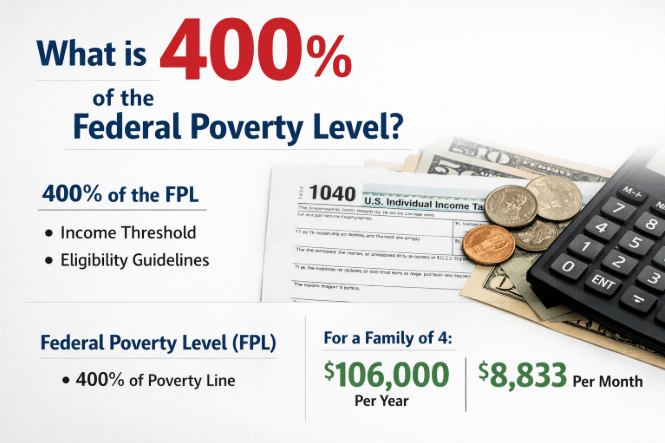

What Is 400% of the Federal Poverty Level: Income Limits, ACA Subsidies and Who Qualifies

400% of the federal poverty level (FPL) is four times the annual poverty guideline published each January by the U.S. Department of Health and Human Services (HHS). For 2026, that figure ranges from $63,840 for a single person to $132,000 for a family of four in the 48 contiguous states, and it marks the upper income boundary for ACA Marketplace premium tax credit eligibility.

Key Takeaways

- In 2026, 400% of the federal poverty level is $63,840 annually ($5,320/month) for a single person and $132,000 annually ($11,000/month) for a family of four in the 48 contiguous states and Washington, D.C.

- The ACA Marketplace subsidy cliff returned on January 1, 2026. Households with income above 400% of the prior year’s federal poverty level are no longer eligible for federal premium tax credits, the enhanced subsidies under the American Rescue Plan Act (ARPA) expired on December 31, 2025.

- ACA Marketplace eligibility for 2026 is calculated using the 2025 federal poverty guidelines, not the 2026 figures. A household comparing its 2026 income against the 2026 HHS table for Marketplace purposes is using the wrong base year.

What Is 400% of the Federal Poverty Level in 2026?

400% of the 2026 federal poverty guidelines range from $63,840 annually for a single person to $132,000 for a family of four in the 48 contiguous states and Washington, D.C. The full 2026 breakdown by household size, annual income and monthly equivalent is in the table below.

2026 Federal Poverty Guidelines at 400%: Annual and Monthly Income

| Household Size | Annual Income (400% FPL) | Monthly Equivalent |

|---|---|---|

| 1 | $63,840 | $5,320 |

| 2 | $86,560 | $7,213 |

| 3 | $109,280 | $9,107 |

| 4 | $132,000 | $11,000 |

| 5 | $154,720 | $12,893 |

| 6 | $177,440 | $14,787 |

| 7 | $200,160 | $16,680 |

| 8 | $222,880 | $18,573 |

Source: HHS Office of the Assistant Secretary for Planning and Evaluation (ASPE), 2026 poverty guidelines. Figures apply to the 48 contiguous states and Washington, D.C.

Alaska and Hawaii carry higher poverty guidelines to reflect the elevated costs of living. For a single person in Alaska, 400% FPL in 2026 is $79,800. For Hawaii, the figure is $73,440. Each additional household member adds $19,920 in Alaska and $18,300 in Hawaii.

These figures apply to most federal and state program determinations. ACA Marketplace subsidy eligibility uses a different base year, the 2025 poverty guidelines, which produces slightly lower dollar thresholds.

How to Calculate 400% of the Federal Poverty Level?

Calculating 400% of the FPL for your household takes four steps, and the fourth is the one most readers get wrong.

- Step 1: Identify your household size. Count every person included in your tax household, including yourself, your spouse if filing jointly, and all dependents you claim.

- Step 2: Find the 100% FPL figure for your state. Go to the HHS ASPE poverty guidelines table for your coverage year. Use the figure listed under your household size. For the 48 contiguous states, the 2026 guideline for a single person is $15,960. For a family of four, it is $33,000.

- Step 3: Multiply by 4. That calculation produces 400% of the FPL for your household. A family of three: $27,320 × 4 = $109,280.

- Step 4: Confirm which base year applies to your program. This is the step that trips up the most readers. Two different 400% FPL figures circulate for 2026 and both are correct, for different purposes.

- $62,600 (single person): 400% of the 2025 HHS poverty guideline. This is the figure used to determine ACA Marketplace premium tax credit eligibility for 2026 coverage, because Marketplace eligibility is always calculated against the prior year’s guidelines.

- $63,840 (single person): 400% of the 2026 HHS poverty guideline. This figure applies to most other federal and state program determinations that use the current year’s guidelines.

Using the 2026 figure to assess your ACA Marketplace subsidy eligibility produces an income threshold that is $1,240 higher than the one the Marketplace actually applies.

A household of one earning $63,000 would fall below the Marketplace’s actual 2026 subsidy threshold of $62,600, and might incorrectly conclude they do not qualify for premium tax credits at all.

Income types counted toward your household total for this calculation include wages, self-employment income, investment income, rental income, and most taxable income. Social Security benefits count toward MAGI in most cases.

For recent changes affecting Social Security payment amounts, see the Social Security Fairness Act payments update.

The ACA Subsidy Cliff: What 400% FPL Means for Health Insurance in 2026?

As of January 1, 2026, households with income above 400% of the prior year’s federal poverty level are ineligible for federal premium tax credits on the ACA Marketplace. The subsidy cliff has returned after a five-year suspension, and a significant share of current Marketplace enrollees are encountering it for the first time.

The ACA subsidy cliff is a binary income cutoff at 400% of the prior year’s FPL. One dollar above the threshold eliminates 100% of premium tax credit eligibility, not a gradual reduction.

A household of two earning $85,000 sits at 402% of the 2025 FPL and receives zero federal subsidy assistance in 2026, while an identical household earning $84,000 (399%) may receive thousands of dollars in annual premium tax credits.

The American Rescue Plan Act (ARPA) eliminated this cliff in 2021. The Inflation Reduction Act (IRA) extended that elimination through 2025. Under those temporary rules, no household paid more than 8.5% of income for the benchmark Silver plan, regardless of income level.

Congress did not extend those provisions. For households with income just above the 400% FPL threshold, reducing ACA-specific MAGI through pre-tax contributions remains the most direct path back to subsidy eligibility.

A Common Misconception Worth Correcting

HealthCare.gov currently states that income above 400% FPL may still qualify for the premium tax credit, that information reflects the expired ARP/IRA rules from 2021–2025 and is no longer accurate for 2026.

As of January 1, 2026, income above 400% FPL renders a household ineligible for federal premium subsidies under the reinstated original ACA structure (ARPA, Section 9661). The enhanced provisions expired on December 31, 2025, and Congress did not extend them.

Expiration confirmed by healthinsurance.org subsidy analysis, updated May 2026. The table below shows exactly how ACA eligibility and cost-sharing access breaks down by income band in 2026.

2026 ACA Marketplace Eligibility by Income Band

| Income Band | Premium Tax Credit | Cost-Sharing Reductions | Notes |

|---|---|---|---|

| 100%–138% FPL | Eligible | Eligible (Silver plans) | Medicaid available in expansion states above 138% |

| 138%–250% FPL | Eligible | Eligible (Silver plans) | Strongest CSR benefits below 200% FPL |

| 250%–400% FPL | Eligible | Not eligible | Premium tax credit only, no deductible or copay reductions |

| Above 400% FPL | Not eligible | Not eligible | Full unsubsidized premium applies, no federal assistance |

A critical point the table makes visible: households between 250% and 400% FPL retain premium tax credit eligibility but lose all access to cost-sharing reductions (CSRs). CSRs lower deductibles, copayments, and out-of-pocket maximums on Silver plans, their absence significantly increases total healthcare costs even when premium subsidies remain.

For enrollees in this band, a Silver plan remains the most cost-effective option, even without CSRs, Silver premiums typically sit below Gold while offering better catastrophic protection than Bronze.

For households with income just above the 400% FPL threshold, reducing ACA-specific modified adjusted gross income (MAGI) through pre-tax Health Savings Account (HSA) contributions or traditional retirement account contributions can restore premium tax credit eligibility entirely.

Federal Programs That Use the 400% FPL Threshold

The ACA Marketplace premium tax credit is the primary federal program that uses 400% FPL as a hard eligibility ceiling. Most other federal programs operate at significantly lower FPL percentages, and knowing which threshold applies to which program prevents a costly misreading of eligibility.

Two terms that appear interchangeably across the web are not actually the same measure. The federal poverty guidelines, published by HHS each January, are the figures used for program eligibility determinations.

They are not the same as the federal poverty thresholds published annually by the Census Bureau, which are used to produce official poverty statistics. The two measures differ slightly in dollar value and methodology.

Program eligibility, including ACA subsidies, Medicaid, and CHIP, always references HHS guidelines, not Census Bureau thresholds.

Key FPL thresholds by program:

- ACA Marketplace Premium Tax Credit:100% to 400% FPL (2026 uses 2025 FPL base). Below 138% FPL in Medicaid expansion states, Medicaid eligibility applies instead.

- Medicaid (expansion states): Up to 138% FPL for most adults. As of 2026, 40 states and Washington, D.C. have expanded Medicaid. The 138% FPL floor marks the Medicaid expansion eligibility threshold.

- Children’s Health Insurance Program (CHIP): Eligibility varies by state, commonly up to 200% FPL for children. Some states extend coverage higher. Children are evaluated separately from adults in the same household.

- SNAP (Supplemental Nutrition Assistance Program): Gross income limit of 130% FPL. Net income limit of 100% FPL. SNAP uses 130% of the FPL as its gross income limit, a threshold currently under active policy review, with USDA to require all SNAP beneficiaries reapply for benefits among the recent changes affecting enrolled households.

- LIHEAP (Low Income Home Energy Assistance Program): Typically up to 150% FPL, varying by state.

400% FPL marks a ceiling for ACA subsidies only. It is not a qualifying threshold for Medicaid, SNAP, CHIP, or LIHEAP, all of which use significantly lower income limits. Assuming 400% FPL eligibility transfers across all assistance programs is one of the most common eligibility misreadings on this topic.

Eligibility for federal assistance programs also depends on factors beyond income. Citizenship status and immigration classification affect access to certain programs. For current guidance on that dimension, see SNAP benefits immigration status guidance.

400% FPL in 2026: What Changed and Why It Matters?

The American Rescue Plan Act temporarily removed the 400% FPL subsidy ceiling from 2021 through 2025. Congress did not extend those provisions.

The original ACA cliff reinstated on January 1, 2026, the most significant Marketplace eligibility change in five years, affecting millions of current enrollees who had been covered under the enhanced subsidy rules since 2021.

Before 2021, the ACA subsidy cliff had existed since the Marketplace opened in 2014. Under original ACA rules, a household of two earning $85,000, equal to 402% of the 2025 FPL, paid the full unsubsidized premium with no health insurance premium subsidy available.

From 2021 through 2025, that same household qualified for subsidies if premiums exceeded 8.5% of income. On January 1, 2026, the subsidy disappeared, for many older enrollees, that meant premium increases of $400 to $1,200 per month.

According to healthinsurance.org, more than 1.6 million people who reported income above 400% FPL during the 2025 open enrollment period are now ineligible for federal subsidies in 2026.

Enrollees aged 55–64 are hardest hit, unsubsidized premiums for a 60-year-old can reach 20%–30% of household income in high-premium states. Healthinsurance.org’s May 2026 subsidy analysis and HHS ASPE 2026 poverty guidelines confirm these figures.

If your income is near the 400% FPL boundary, reducing your ACA-specific MAGI below the threshold through pre-tax HSA contributions (2026 individual limit: $4,300), traditional IRA contributions (2026 limit: $7,000), or 401(k) contributions (2026 limit: $23,500) can restore full premium tax credit eligibility.

Any advance premium tax credits received are reconciled on IRS Form 8962 at tax filing. If income exceeded 400% FPL for the year, the full credit amount must be repaid.

Conclusion

This threshold is precise, annually updated, and in 2026, it carries more real-world weight than at any point since 2020. The subsidy cliff’s return means households above the threshold pay the full unsubsidized Marketplace premium.

Knowing which base year applies and managing MAGI accordingly can be worth thousands of dollars annually. 400% of the federal poverty level means the hard boundary between subsidized and unsubsidized health coverage for millions of American households in 2026.

FAQ

What is 400% of the federal poverty level for a family of 4 in 2026?

$132,000 per year or $11,000 per month. This figure is based on the 2026 HHS poverty guideline of $33,000 for a family of four, multiplied by four. For ACA Marketplace subsidy purposes, the 2025-based figure of $128,600 applies instead.

Does 400% FPL still apply to ACA subsidies in 2026?

Yes, the 400% FPL income cap is fully reinstated for 2026. The enhanced subsidies under the American Rescue Plan Act expired on December 31, 2025. Households with income above 400% of the prior year’s FPL receive no federal premium tax credit assistance in 2026.

What is the difference between the 400% FPL subsidy cliff and a gradual phase-out?

The cliff is binary, not gradual. One dollar above the 400% FPL threshold eliminates 100% of premium tax credit eligibility, not a proportional reduction. From 2021 through 2025, a gradual phase-out replaced the cliff. That structure expired in 2026, and the binary hard cutoff is now reinstated.

Which year’s federal poverty guidelines are used for 2026 Marketplace eligibility?

The 2025 federal poverty guidelines are used for 2026 ACA Marketplace premium tax credit eligibility, not the 2026 guidelines. This means the relevant 400% FPL threshold for a single person’s 2026 Marketplace subsidy determination is $62,600, not the 2026 figure of $63,840.

What is the federal poverty level for a single person in 2026?

$15,960 per year for a single person in the 48 contiguous states and Washington, D.C., based on the 2026 HHS poverty guidelines. At 400%, that equals $63,840 annually or $5,320 per month.

What is the difference between federal poverty guidelines and federal poverty thresholds?

Federal poverty guidelines published by HHS determine eligibility for programs including ACA subsidies, Medicaid, and SNAP. Federal poverty thresholds published by the Census Bureau are used solely for official poverty statistics. All program eligibility uses HHS guidelines, not Census Bureau thresholds.

Who qualifies for federal assistance programs based on FPL?

Eligibility depends on the specific program, household size, state of residence, and income as a percentage of FPL. Medicaid expansion covers adults up to 138% FPL in most states. ACA premium tax credits cover households from 100% to 400% FPL. Eligibility also depends on citizenship and immigration status see SNAP benefits immigration status guidance for current federal guidance on that dimension.

Disclaimer: This article is for informational purposes only — verify current figures and eligibility rules at HHS.gov or HealthCare.gov before making any coverage decisions.