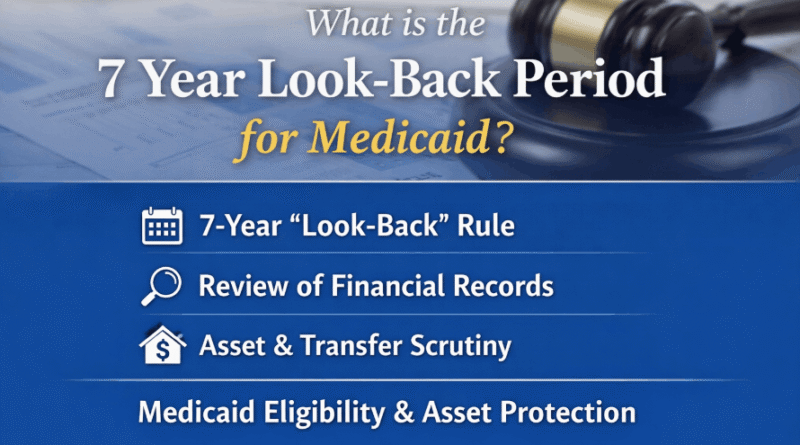

What Is the 7 Year Look-Back Period for Medicaid? The 2026 Audit Guide

Technically, there is no federal 7 year look-back period for Medicaid; the standard look-back period is 60 months (5 years) in nearly every state.

The 7-year term is a common misconception often conflated with IRS estate tax windows or private long-term care insurance (LTCI) elimination periods.

According to the Centres for Medicare & Medicaid Services (CMS) guidelines, any assets gifted or sold below Fair Market Value within the 60 months prior to your Medicaid application will trigger a transfer penalty, delaying your coverage for long-term care.

Key Takeaways

- The Federal Standard: Most states utilize a 60-month (5-year) look-back period for nursing home Medicaid.

- The 7-Year Origin: This figure typically stems from confusion with IRS Look-back rules for estate taxes or outdated private insurance terminology.

- 2026 State Variances: California reinstated a modified asset test and 30-month look-back on January 1, 2026, while New York continues to delay its Community Medicaid look-back.

- Penalty Impact: Transfers made within the look-back window result in a period of ineligibility based on the regional cost of care.

What is the 7 year look-back period for Medicaid?

While many applicants ask, what is the 7 year look-back period for Medicaid, federal law under the Deficit Reduction Act of 2005 (DRA) strictly mandates a 60-month (5-year) audit window.

During this time, state Medicaid agencies review all financial records to ensure you have not divested assets to qualify for assistance.

The look-back period begins the moment you apply for Medicaid and are otherwise eligible for nursing home care.

If you transferred a home, cash, or investments for less than they were worth between 2021 and 2026, those transactions are now under regulatory scrutiny.

Only in very specific, non-standard estate planning scenarios, usually involving complex trusts or private insurance, does a seven-year timeline ever enter the conversation.

State Audit Deviations from Federal Look Back Rules

Understanding why the 7-year figure persists is essential for any applicant attempting to navigate the 60-month federal reality. This misconception typically stems from three specific regulatory overlaps.

- IRS Estate Tax Conflation: The IRS often looks back through a seven-year window for certain gifts made in contemplation of death regarding large taxable estates. Individuals often confuse tax law with social welfare eligibility.

- Look-back vs. Penalty Period: While the audit (look-back) is 5 years, the penalty (disqualification) has no upward limit. If you gifted $1,000,000 in 2024, your penalty period could technically last 10 years or more, leading to the 7-year myth.

- Private Long-Term Care Insurance: Some older private policies utilized a 7-year elimination period or specialized benefit triggers that required historical records dating back further than the federal Medicaid standard.

Applicants must be prepared to provide 60 months of consecutive bank statements for every open and closed account held by either spouse; the look-back is an exhaustive financial reconstruction, not a simple review.

Debunking Common Asset Scrutiny Myths

| The Myth | The Regulatory Reality (2026) |

| Medicaid looks back 7 years. | The federal look-back is exactly 60 months. |

| I can gift $19,000 per year per IRS rules. | Any gift, regardless of IRS limits, triggers a Medicaid penalty. |

| The look-back only applies to cash. | It applies to real estate, vehicles, and business interests. |

| Only large transfers are audited. | Auditors check for patterns of small cash withdrawals. |

Why IRS Gift Limits Trigger Medicaid Penalties?

A critical oversight in most financial advice is the failure to distinguish between IRS gifting limits and Medicaid eligibility. While the IRS allows for tax-free transfers, Medicaid regulators view those same transactions as disqualifying divestments.

In 2026, the IRS allows you to gift up to $19,000 per person without filing a gift tax return (Form 709). However, Medicaid does not recognize this exclusion.

According to CMS State Medicaid Manual Section 3258.1, any transfer for less than Fair Market Value is considered a divestment, even if it is legally tax-free under the IRS code.

If you gift $19,000 to five grandchildren, you have created a $95,000 Medicaid transfer penalty. Auditors specifically cross-reference IRS filings to identify these uncompensated transfers during the 60-month window.

Any property transfer for less than Fair Market Value (FMV) is legally classified as an uncompensated transfer, regardless of the relationship between the grantor and the recipient.

Funding Requirements For Asset Protection Trusts

To secure assets, many utilize Medicaid asset protection trust rules. To be effective, a Medicaid Asset Protection Trust (MAPT) must be irrevocable, and the grantor (you) cannot have access to the principal.

To bypass the 60-month look-back, a MAPT must be fully funded and the look-back window must expire before the first application for benefits is filed.

Because the transfer into the trust is considered a gift, it must occur at least 60 months before you apply for Medicaid.

If you fund a MAPT and require care 59 months later, the entire trust value is subject to a transfer penalty. Furthermore, retained rights to income from the trust can affect eligibility, even if the principal is protected.

Current Medicaid Look Back Periods By State

While the federal government sets the floor, states have the authority to adjust look-back periods for specific types of care. As of 2026, several states have significantly adjusted their thresholds.

| Care Type | Federal Standard | California (2026) | New York (2026) |

| Nursing Home Care | 60 Months | 30 Months (Reinstated) | 60 Months |

| Community / At-Home | 0 Months | 0 Months | 0 Months (Delayed) |

| Asset Limit (Indiv.) | $2,000 | $130,000 | $32,532 |

As of January 1, 2026, California has reinstated specific asset scrutiny protocols. While the $130,000 threshold remains more generous than the federal standard, the new 30-month look-back for institutional care adds a significant layer of complexity for West Coast families.

Calculating the Penalty for Transferring Assets Before Medicaid

The penalty for transferring assets before Medicaid is calculated by dividing the total value of transferred assets by the State Regional Monthly Cost of Care. For example, if you gifted $120,000 and the state’s divisor is $12,000, you are ineligible for Medicaid for 10 months.

To calculate your potential exposure:

- Audit your records: Identify every uncompensated transfer made in the last 60 months.

- Identify the Divisor: Locate the current 2026 monthly divisor for your specific region (e.g., Florida vs. New York).

- Determine the Start Date: The penalty only begins when you are in a nursing home and have exhausted all other assets, not on the date the gift was made.

What is Exempt from Medicaid Look-back?

Certain transfers are protected from the Medicaid 5 year look back rule exceptions if they meet federal Safe Harbor criteria.

- The Caregiver Child Exception: You may transfer your primary residence to a child who lived in the home for at least two years prior to your institutionalization and provided care that delayed your entry into a facility.

- Sibling with Equity Interest: Transfer is permitted to a sibling who has an equity interest in the home and lived there for at least one year.

- Transfers to Disabled Individuals: Assets transferred to a blind or permanently disabled child (or a trust for their sole benefit) are generally exempt from penalties.

The Penalty Trigger and Timing Rule

The Medicaid penalty period does not begin on the date an asset was gifted; instead, it triggers only after an applicant is residing in a nursing home, has applied for Medicaid, and is otherwise eligible except for the transfer.

This regulatory gap means a gift made four years ago can result in a disqualification period that only starts years later, potentially leaving the individual with no means to pay for care.

Compliance Protocols For 2026 Redeterminations

If you find yourself within the look-back window with excess assets, you must follow Spend-down protocols rather than gifting.

- Debt Liquidation: Pay off mortgages or credit cards.

- Home Improvements: Use liquid cash to increase the value of your exempt primary residence.

- Prepaid Funerals: Purchase an Irrevocable Funeral Trust.

Managing high income alongside asset concerns often requires a broader look at welfare thresholds. Those navigating this balance may find a useful baseline in our analysis: If I make $1,800 a month can I get Food Stamps.

Conclusion

The 7 year look-back period for Medicaid is a persistent myth; the reality is a strictly enforced 60-month federal audit.

For 2026, applicants must reconcile IRS gifting allowances with CMS divestment penalties to avoid devastating gaps in care coverage. Always verify current regional divisors with your state’s Medicaid agency before transferring title to any property.

What is the 7 year look back period for Medicaid means understanding the 60-month federal audit window for seniors and families in 2026.

FAQ

Does Medicaid check my bank account without permission?

No, but they require you to provide the statements as a condition of eligibility. Failure to provide 60 months of records results in an automatic denial.

What triggers a Medicaid audit in 2026?

The application itself triggers the audit. However, large even-dollar withdrawals (e.g., $5,000) or a sudden closure of investment accounts will prompt a Request for Information (RFI) from the caseworker.

How many bank statements do I need for Medicaid?

You must provide 60 months of statements for all checking, savings, and investment accounts. Auditors look for even-dollar withdrawals or patterns of cash transfers that suggest gifting.

Does Medicaid look at cash withdrawals?

Yes, any withdrawal over a specific state-mandated threshold (often as low as $500) that cannot be documented with a receipt for goods or services is treated as a penalized gift.

What triggers a Medicaid investigation?

Inconsistencies between reported income on tax returns and bank deposits, or the sudden closure of life insurance policies with cash value, are primary triggers for a secondary eligibility investigation.

Can I sell my house for $1.00 to my kids?

No. This is a classic uncompensated transfer. Medicaid will treat the difference between $1.00 and the Fair Market Value as a gift, triggering a massive penalty.

Do small holiday gifts count?

Technically, yes. While some caseworkers ignore “de minimis” gifts (under $500), a series of $1,000 Christmas gifts over five years can accumulate into a month of lost coverage.

What happens if I win the lottery while on Medicaid?

A lottery win constitutes a ‘change in circumstances.’ Regulatory protocol requires you to report the windfall immediately to the Social Security Administration (SSA) or your state agency to avoid fraud allegations.