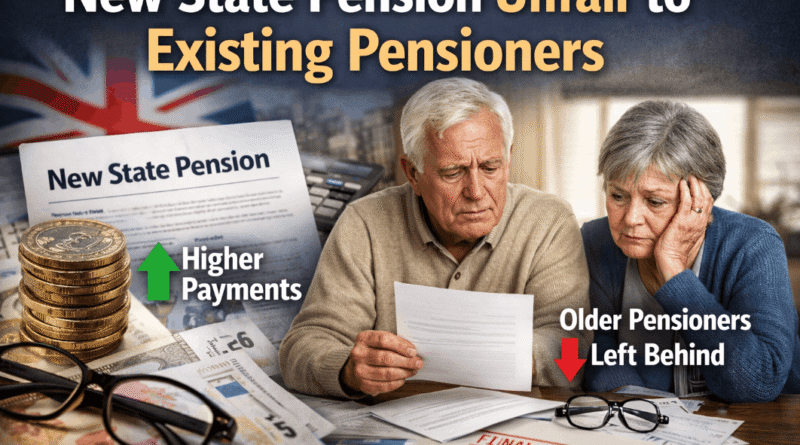

Is the New State Pension Unfair to Existing Pensioners? 2026 Rates, Gaps, and HMRC Tax Traps

The disparity between the old and new state pension systems has become one of the most debated topics in UK personal finance.

As of 2026, the cash gap between those who retired before April 2016 and those who retired after has widened significantly, leading many to argue that the narrative of the new state pension being unfair to existing pensioners is increasingly supported by current economic data.

The UK state pension system transitioned to a single-tier model on 6 April 2016 to simplify retirement income. However, this created a two-tier structure where new pensioners receive a higher weekly flat rate compared to existing pensioners on the basic state pension.

While the Triple Lock applies to both, the different baseline amounts result in a growing annual income divide.

Why is the new state pension unfair to existing pensioners?

The perceived unfairness stems from a structural income gap. In the 2026/27 tax year, the full New State Pension is £241.30 per week, while the full Basic State Pension is £184.90.

This creates a weekly difference of £56.40, meaning existing pensioners receive roughly £2,932 less per year than those under the new system.

At a Glance: The 2026 Pension Divide

| Pension Type | Weekly Rate (2025/26) | Weekly Rate (2026/27) | Annual Total |

| New State Pension | £230.25 | £241.05 | £12,534.60 |

| Basic (Old) Pension | £176.45 | £184.75 | £9,607.00 |

| The Cash Gap | £53.80 | £56.30 | £2,927.60 |

The Financial Reality of the Two-Tier System

The primary grievance for millions of retirees is that the cost of living, heating, food, and transport remains identical regardless of when a person reached state pension age.

In practice, a pensioner who turned 65 in March 2016 faces the same inflationary pressures as one who turned 66 in May 2016, yet their guaranteed state support differs by nearly £3,000 annually.

A common pattern observed in DWP data is that while the Triple Lock provides equal percentage increases (4.7% for April 2026), the higher baseline of the new system results in more new money in absolute terms.

This mathematically ensures the gap never closes; it only expands. To mitigate these rising costs, some individuals may be eligible for specific one-off supports, such as the DWP £750 payment boost in June 2025, which serves as a vital lifeline for those navigating the transition between different benefit systems.

Understanding these auxiliary payments is essential for maintaining household stability in a two-tier landscape.

What is the new state pension?

Replacing the previous web of basic and additional payments, the New State Pension functions as a single-tier foundation for those reaching retirement age on or after 6 April 2016. It replaced the previous complex system of basic and additional pensions with a single-tier amount.

Evolution of the Retirement Benefit

Introduced via the Pensions Act 2014, the system was designed by the Coalition Government to provide a clearer foundation for retirement planning.

To qualify for any payment, individuals usually need 10 qualifying years on their National Insurance record, with 35 years required to receive the full flat-rate amount.

Quick Eligibility Check: Which System Are You In?

- Old Basic System: Men born before 6 April 1951; Women born before 6 April 1953.

- New Single-Tier System: Men born on/after 6 April 1951; Women born on/after 6 April 1953.

Why did the government introduce the new state pension?

The previous system was widely criticised for being overly complicated and reliant on means-testing. By introducing a higher flat-rate amount, the government aimed to:

- Simplify planning: Making it easier for workers to see exactly what they would receive.

- Reduce means-testing: Ensuring the state pension alone stayed above the level of basic Pension Credit.

- Incentivise private saving: Providing a solid base so people know their private pensions wouldn’t just result in a loss of state benefits.

When and who introduced the new state pension?

Steve Webb, the Pensions Minister during the Coalition era, drove the 2014 reforms with the intention of modernising what was then considered a fractured system.

It is a common misconception that the new pension was a gift; for many, it involved the removal of the State Second Pension (S2P) and SERPS, which were additional earnings-related top-ups available under the old rules.

Myth vs Reality on New State Pension

Many retirees feel the new system is an automatic windfall, but the reality is more nuanced.

| Feature | Common Misconception | 2026 Reality |

| Eligibility | Everyone gets the full £241.30. | Only those with 35 full NI years and no contracting-out history get the full rate. |

| Savings | Your NI contributions are held in a personal pot. | NI is a pay-as-you-go tax; today’s workers pay for today’s pensioners. |

| Fairness | Old pensioners are always worse off. | Some old pensioners with high SERPS earn more than the New State Pension maximum. |

| Inflation | The Triple Lock fixes the gap. | Percentage increases cause the cash gap to widen every year. |

The Contracted Out Reality: Why New is not always better

When reviewing decisions made in the 1980s and 1990s, many workers chose to contract out of the Additional State Pension. In exchange, they paid lower National Insurance or diverted funds into a private scheme.

For example, David, who retired in 2024, was shocked to find his New State Pension was lower than the headline rate. This is because a Contracted Out Pension Equivalent (COPE) adjustment was made to his record.

Conversely, Margaret, who retired in 2012, receives a Basic Pension plus a significant SERPS payment, actually bringing her total weekly income above the New State Pension cap. This hidden parity is often overlooked in the fairness debate.

Practical Steps: Managing your pension in 2026

Navigating the complexities of the 2016 transition requires a proactive approach to managing your DWP record.

- Check your State Pension forecast: Use the Check your State Pension service on GOV.UK to see your projected amount.

- Review your NI record: Identify any partial years that could be filled to increase your payment.

- Apply for a BR19 form: If you prefer paper statements, this provides a detailed breakdown of your record.

- Identify Contracted Out periods: Look for years where you paid into a workplace scheme that may reduce your state total.

- Verify Pension Credit eligibility: If your income is below £218.15 (single) or £332.95 (couple), you may be entitled to a top-up.

- Report changes immediately: Notify the DWP of any change in address or bank details to avoid payment interruptions.

- Seek free advice: Use services like MoneyHelper or Citizens Advice rather than paid third parties.

When should I worry about my state pension?

You should focus on your pension status if you have fewer than 10 years of National Insurance contributions, as you may receive nothing at all. Additionally, those approaching age 66 should check their forecast at least two years in advance.

Gaps in your record can often be bridged by paying voluntary Class 3 NI contributions, but there are strict time limits (usually six years) on how far back you can go.

Who owns the new state pension and who should I approach?

Under the jurisdiction of the Department for Work and Pensions (DWP), the system is managed day-to-day by The Pension Service.

No private company owns or manages this benefit. If you encounter issues, such as missing payments or incorrect forecasts, you should contact the Future Pension Centre (if you haven’t reached pension age) or the Pension Service (if you have).

Do I need to pay to make changes?

There is no requirement to pay for administrative changes. Correcting your details, claiming your entitlement, or updating your file with the DWP are entirely free services. Be wary of any website or service charging a fee to speed up your application or calculate your increase.

The 2026 Tax Threshold Trap

A significant development in 2026 is the convergence of the New State Pension and the Personal Tax Allowance. With the tax-free threshold frozen at £12,570, the 4.8% increase in the state pension brings the full new rate to approximately £12,548 per year.

This leaves a razor-thin margin of just £22 in headroom before the average retiree is pulled into the tax net.

Beyond the state-provided income, individuals must also navigate broader fiscal traps; for instance, HMRC warns that savings over £3,501 may incur tax if interest earnings exceed the personal savings allowance, potentially creating an unexpected liability for those with modest nest eggs.

Existing pensioners on the lower rate have more headroom, but less disposable income, adding another layer to the complexity of what is considered fair.

FAQ about new state pension unfair to existing pensioners

Why do people on the old pension get less money?

The old system was built on a lower base rate supplemented by earnings-related additions (SERPS). Many existing pensioners did not accrue these additions, leaving them with only the basic rate, which is lower than the new single-tier flat rate.

Can I switch from the old state pension to the new one?

No. Your state pension age determines which system you fall into. If you reached state pension age before 6 April 2016, you remain on the old system for life; there is no option to opt in to the new rates.

Does the Triple Lock apply to both pensions?

Yes, the Triple Lock applies to both the Basic State Pension and the New State Pension. However, because it is a percentage-based increase, the cash gap between the two amounts grows larger every year.

What is the protected payment in the new state pension?

If your NI record under the old rules entitled you to more than the new full flat rate, the difference is paid as a protected payment. This ensures that no one is worse off at the point of transition.

Is Pension Credit the solution to the unfairness?

For those on the lowest incomes, Pension Credit acts as a safety net, topping up weekly income to a guaranteed minimum level. It also acts as a gateway to the Winter Fuel Payment and Council Tax reductions.

Why did the government change the rules in 2016?

The goal was to create a sustainable, simpler system that reduced reliance on complex means-tested benefits. It was also designed to account for the fact that most people now have workplace pensions through auto-enrolment.

How many years of NI do I need for the full old vs new pension?

Under the old system, you generally needed 30 qualifying years for a full basic pension. Under the new system, you need 35 qualifying years to receive the full flat-rate amount.

Summary of Next Steps

The debate over whether the new state pension unfair to existing pensioners will likely persist as the income gap widens through 2026. While the new system is simpler, the transitional cliff edge has left many older retirees feeling undervalued.

- Audit your income: Ensure you are receiving any SERPS or Graduated Pension you are entitled to.

- Check for credits: If you were a carer or parent, ensure your NI credits were correctly applied.

- Apply for support: If the gap is causing financial hardship, check your eligibility for Pension Credit immediately.