£50k After Tax UK: Your 2026/27 Take-Home Pay, Student Loan Impact, and Tax Threshold Guide

Knowing exactly what you take home on 50k after tax in the UK is vital for financial planning in the 2026/27 tax year.

While earning £50,000 remains a significant professional milestone, frozen tax thresholds and evolving student loan policies mean your actual disposable income is shifting.

While £50k remains well above the national average, fiscal drag means that more of this income is being captured by the tax system than in previous decades.

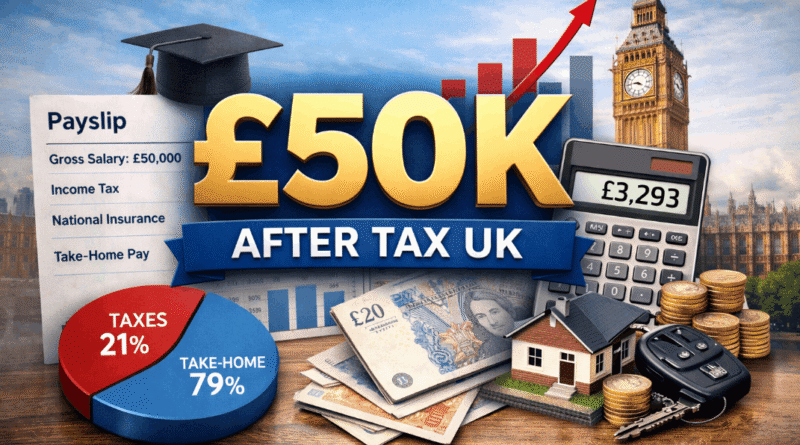

In the 2026/27 tax year, a £50,000 gross salary results in an estimated take-home pay of £39,520 per year for a standard taxpayer in England, Wales, or Northern Ireland. This breaks down to approximately £3,293 per month.

This breakdown explains your net pay, National Insurance, and the ‘higher rate trap’ for the 2026/27 tax year.

Calculated Breakdown: 50k After Tax UK 2026/27

For most employees using the standard 1257L tax code, here is the foundational breakdown of a £50,000 salary for the 2026/27 tax year.

| Period | Gross Income | Income Tax (20%) | National Insurance (8%) | Take-Home Pay |

| Yearly | £50,000 | £7,486 | £2,994 | £39,520 |

| Monthly | £4,166.67 | £623.83 | £249.50 | £3,293.33 |

| Weekly | £961.54 | £143.96 | £57.58 | £760.00 |

| Daily (8hr) | £192.31 | £28.79 | £11.51 | £152.00 |

| Hourly | £24.04 | £3.60 | £1.44 | £19.00 |

Keep in mind that these figures represent your take-home pay before the standard 5% auto-enrolment pension deduction is applied.

2026/27 Take-Home Pay by Pension Contribution

| Pension Contribution | Annual Take-Home | Monthly Take-Home | Monthly Pension Cost |

| No Pension (0%) | £39,520 | £3,293 | £0 |

| Standard (5%) | £37,520 | £3,126 | £166 |

| High (10%) | £35,520 | £2,960 | £333 |

How Much of Your £50k Goes to the Government?

When you earn £50,000, the government takes exactly £10,480 per year from your salary through two primary channels. This means approximately 21% of your total gross income is paid directly to the state before you receive your take-home pay.

- Income Tax: You pay 0% on your first £12,570 (Personal Allowance) and 20% on the remaining £37,430.

- National Insurance (NI): For 2026, the main rate of Class 1 NI for employees is 8%. You pay this on earnings above the Primary Threshold of £12,570 per year.

In total, you contribute over £10,480 per year toward public services and the state pension before any other voluntary or statutory deductions. All tax bands and thresholds are based on official HMRC guidance for the 2026/27 tax year.

The Government’s Share: Annual Cost Breakdown

| Deduction Type | Annual Amount | Monthly Impact |

| Income Tax (PAYE) | £7,486.00 | £623.83 |

| National Insurance | £2,994.00 | £249.50 |

| Total Government Take | £10,480.00 | £873.33 |

The 2026 Personal Allowance and the Fiscal Drag Effect

The tax-free Personal Allowance remains frozen at £12,570, a level it has held since 2021. This phenomenon, known as Fiscal Drag, means that as wages rise with inflation, a larger portion of your real income is taxed because the tax-free bucket hasn’t grown.

Understanding this is crucial for anyone whose salary has recently reached the £50k mark.

Those planning for future career growth should also consider how this impact accelerates as earnings increase; for example, seeing an 80k salary after tax in the UK highlights a much more aggressive tax take as a higher percentage of income enters the 40% bracket.

Is £50,270 still the magic number for the higher tax bracket?

Yes. In 2026, the threshold for the 40% Higher Rate tax remains £50,270. At a £50,000 salary, you are sitting just £270 below the point where the government starts taking 40p of every extra pound you earn.

Do you pay 40% tax on the whole £50,000?

No. This is a common myth. You only pay 40% on the portion of your income that exceeds £50,270. On a £50,000 salary, every taxable pound you earn is still taxed at the 20% Basic Rate.

The Higher Rate Trap: Why £51k Can Feel Worse Than £49k

While £50k is a comfortable ceiling, crossing it can trigger the High Income Child Benefit Charge (HICBC).

- From April 2024, the threshold for this charge was increased to £60,000.

- If you earn between £60,000 and £80,000, your Child Benefit is gradually clawed back.

- At £50,000, you are currently safe from this specific trap, but a significant pay rise or bonus could suddenly make your net income feel smaller if you have a family.

For those targeting a major promotion, exploring the take-home pay on 70k After Tax UK illustrates how the interaction of higher-rate tax and benefit clawbacks changes your actual “net” gains as your career progresses.

High earners approaching the £60,000 mark frequently utilise Salary Sacrifice to manage their pension contributions. Comparing your earnings to a salary of 60k after tax UK reveals how reducing your Adjusted Net Income protects Child Benefit while building tax-free wealth.

Why Your Take-Home Might Be Lower Than Expected

If your payslip doesn’t match the clean numbers above, it is likely due to one of these three variables:

- Student Loans: Repayments depend on your specific plan. On Plan 2 (threshold £28,470), you’ll see a monthly deduction of roughly £161. However, those on the newer Plan 5 face a lower £25,000 threshold, meaning a higher monthly cost of £187.

- Pension Contributions: Most employers use a 5% auto-enrolment rate. This is deducted before tax, which is excellent for long-term wealth but reduces your monthly liquid cash.

- HMRC Underpayments: If you have shifted jobs or have a company benefit (like private health insurance), HMRC may adjust your tax code (e.g., to 1100L), resulting in slightly higher tax deductions until the balance is cleared.

The Bonus Tax and Company Perks

Why is a bonus on a £50k salary taxed so heavily?

If you receive a £1,000 bonus, that entire amount sits above the £50,270 threshold (if your base is £50k). This means it is taxed at the 40% Higher Rate, plus National Insurance and potential Student Loan repayments. You might only see £450–£500 of that £1,000 in your bank account.

£5,000 Bonus Scenario

If you receive a £5,000 annual bonus on top of your £50,000 salary, it is taxed at the 40% higher rate. After 40% Income Tax (£2,000) and 8% National Insurance (£400), your net bonus is £2,600. If you have a Student Loan (9%), a further £450 is deducted, leaving you with £2,150 from the original £5,000.

The Company Car Effect

If your employer provides a company car, HMRC treats this as a “Benefit in Kind” (BiK). The taxable value of the vehicle is added to your salary, which can inadvertently push your total income into the 40% bracket.

Regional Differences: £50k in Scotland vs. England

Scottish taxpayers on £50,000 face a different reality. The Scottish Government utilizes a more granular system where the Higher Rate (42%) starts at just £43,663.

- Take-Home in London: ~£39,520

- Take-Home in Glasgow: ~£37,800

Scottish earners on £50k take home roughly £1,700 less per year than their counterparts elsewhere in the UK.

Living on £50k: Now and in 2030

Is £50,000 a good salary? In 2026, it remains comfortably above the UK median, but its purchasing power is declining.

- The 2030 Outlook: At a 3% average inflation rate, £50,000 in 2030 will have the same purchasing power as approximately £44,000 today.

- Single Person: Generally provides a high quality of life, allowing for city-center living and consistent savings.

- Parents with Children: In 2030, a single-income household on £50k will likely feel the middle-class squeeze, with most of the income consumed by housing, energy, and childcare.

This financial pressure is intensified by the current cost of borrowing. Monitoring the UK interest rate forecast for next 5 years is essential, as rising debt costs erode the disposable income of a £50k salary.

Strategic Financial Planning for £50k Earners

Freelance vs. PAYE

If you earn £50,000 as a freelancer, your tax is handled via Self-Assessment. While you can deduct expenses, you miss out on employer pension contributions (worth at least £1,500/year) and sick pay. Generally, a £50k PAYE salary is more valuable than £50k in freelance billings.

2026 ISA Strategies

On a £50k salary, you likely have surplus cash. Utilizing a Stocks & Shares ISA or a Cash ISA is vital. Since the personal savings allowance for basic rate taxpayers is £1,000, but drops to £500 for higher rate taxpayers, using an ISA ensures your interest and dividends remain 100% tax-free even if you receive a pay rise.

Maximising Income with the Marriage Allowance

If you are married or in a civil partnership, you may qualify for the Marriage Allowance. This allows a lower-earning partner (earning below £12,570) to transfer £1,260 of their Personal Allowance to the higher earner.

For a £50,000 earner, this reduces the annual tax bill by up to £252. To qualify, the higher earner must be a basic-rate taxpayer, which fits perfectly for those earning exactly £50,000 before crossing the higher-rate threshold.

FAQ about 50k after tax UK

What is the monthly take-home pay on £50k after all deductions?

In 2026/27, a £50k salary nets approximately £3,293 per month before voluntary deductions. After a standard 5% pension contribution, your take-home pay is roughly £3,126. These figures account for the 20% basic rate Income Tax and 8% National Insurance.

How much is £50,000 an hour after tax?

Based on a 37.5-hour week, your gross hourly rate is £25.64. After 2026/27 tax and National Insurance, your net hourly pay is £20.26. This amount decreases if you have student loan repayments or pension contributions.

Is £50,000 enough to qualify for a Skilled Worker Visa in 2026?

Yes, £50,000 exceeds the general £41,700 Skilled Worker Visa threshold for 2026. However, you must also meet the specific going rate for your job code. If your occupation requires a higher minimum, £50k may be insufficient for sponsorship.

Why is my take-home pay lower than the online calculator said?

Calculators often omit specific deductions. Your pay might be lower due to Student Loans (9%), higher pension contributions, or taxable benefits like medical insurance. These benefits often result in a reduced tax code, increasing your monthly tax bill.

Combined Deduction Scenario: The Real World £50k Payslip

Many professionals in 2026 fall into the triple deduction category: paying Income Tax, National Insurance, a Student Loan, and a workplace pension. Here is how that looks for a standard Plan 2 borrower with a 5% pension contribution.

| Item | Monthly Amount | Annual Total |

| Gross Salary | £4,166.67 | £50,000.00 |

| Income Tax (20%) | – £623.83 | – £7,486.00 |

| National Insurance (8%) | – £249.50 | – £2,994.00 |

| Pension (5% on Qualifying Earnings) | – £145.87 | – £1,750.40 |

| Student Loan (Plan 2) | – £155.08 | – £1,861.00 |

| Final Take-Home (X) | £2,992.39 | £35,908.60 |

The Monthly Milestone: As shown above, once you factor in these common 2026 deductions, a £50,000 salary results in a take-home pay that sits just under the £3,000 per month mark. Effectively, roughly 28% of your gross income is deducted before it reaches your bank account.

What happens to my £50k take-home if I have a company car?

A company car is a Benefit in Kind (BiK) with a taxable value based on emissions. HMRC adds this value to your £50k income, which often pushes you into the 40% tax bracket, increasing the tax due on your cash salary.

Will £50k still be a good salary in 2030?

Currently strong, a £50k salary will have the purchasing power of £44,000 by 2030 due to 3% annual inflation. While comfortable for individuals, families in high-cost areas like London will feel a significant financial squeeze.

How does the 2026 Personal Allowance affect my £50k earnings?

The frozen £12,570 Personal Allowance creates Fiscal Drag. As wages rise, more of your income is taxed because the threshold remains static. This results in a hidden tax increase as a larger percentage of your total pay becomes taxable.

Can I get Universal Credit on a £50,000 salary?

Most £50k earners do not qualify for Universal Credit. However, families with several children and very high housing costs might receive limited support. For most, the high income means the benefit is tapered to zero.

When will the 2026 tax changes actually hit my bank account?

Tax changes take effect on April 6th. Most employees will see updated National Insurance or tax rates in their end-of-April payslip. Weekly-paid workers will see the impact in the first full pay cycle following the new tax year.

How does inflation at 3% devalue a £50k salary over 5 years?

At 3% inflation, your £50k salary loses £1,500 in value annually. By 2031, its purchasing power drops to roughly £43,130. Without pay rises, this significantly reduces what you can afford for housing and general living costs.

Conclusion

A £50,000 salary in 2026 is a financial sweet spot; you are earning well, but are on the precipice of higher tax bands. To maximize this income, focus on pension salary sacrifice to stay efficient and ISA utilization to protect your savings from further tax.